facebook

facebook

Whatsapp

Whatsapp

NAVIGATING DEBT: INSIGHTS FROM FINANCIAL LEADERS IN GUAM AND THE REGION

By Oyaol Ngirairikl and Pauly Suba

Businesses and consumers typically carry debt as a necessity of doing business and leading an engaged life.

For individuals in Guam and the Northern Mariana Islands, credit cards and personal loans are used for vacations, vehicles, educational expenses, and loan consolidation, according to local bankers.

Executive vice president and Guam-CMNI region manager

First Hawaiian Bank

“Debt can be good if used to acquire (high cost) goods or homes,” according to Edward G. Untalan, executive vice president and Guam-CMNI region manager of First Hawaiian Bank and president of the Guam Bankers Association. The average consumer does not have the cash to purchase such large ticket items. Problems arise, however, if “consumers do not manage and pay down the debt (which) could lead to defaults,” he says.

Untalan says consumers and businesses alike have to be smart about what they borrow.

"Rising interest rates over the last year has had an impact on consumer and residential debt," Untalan says.

Senior vice president/chief sales officer

Bank of Guam

When it comes to personal debt, Keven Camacho, senior vice president/chief sales officer of Bank of Guam, says the rough percentage of income going towards personal debt is 13%. He says data from local banks and credit unions, total consumer loans at the end of the fourth quarter of 2023, stood at $840,223,000. Additionally, according to the 2020 Guam Census information, adults 17 years of age and above make up 73% of the population, or 112,300 people. Extrapolating from that data, the average debt per adult on Guam is roughly $7,482. We also know that the Median Household Income is $58,289.

President and CEO

BankPacific

Philip J. Flores, president and chief executive officer of BankPacific, says based on credit scores his institution runs, up to about 30% have a good credit score, which means people are paying their debt in a timely manner. Another 25% have somewhat mediocre scores. “Unfortunately, about 30% to 40% have a poor credit score. The reason for a poor credit score is, a person has too many loans, too many credit cards,” Flores says. “I will sometimes counsel people, and say, if you don't need to borrow money, don't borrow money. If you don't need a new car, why borrow money? Just borrow money for what you need, not for what you want, which is a basic thing in economics.”

President and CEO

Community First Guam Federal Credit Union

Gerard A. Cruz, president and CEO of Community First Guam Federal Credit Union, adds to this picture by illustrating where Guam residents stand among the nation’s borrowers.

“Nationwide, average household debt runs about $100,000, inclusive of mortgage related debt. For our members with mortgages, average household debt is about 30-50% higher. This is due primarily to the higher housing costs as well as the overall higher cost of living,” Cruz says. “The most common source of personal debt is credit card debt, which is generally easier to come by and more difficult to pay off.”

CEO

Coast360 Federal Credit Union

Gener F. Deliquina, CEO of Coast360, says inflation has also contributed to local debt levels.

“Personal debt has increased due to cost-of-living expense due to higher prices in services and goods (inflation), supply and demand, second mortgage financing (where borrowers take advantage of the equity in their home), and higher uses of credit borrowing,” Deliquina says.

This can be a challenge to the local economy as higher debt levels mean consumers are spending more money on debt and spending less in stores. And consumers defaulting on loans can impact the loaning institutions in terms of losses, which could lead to larger issues if the defaults are widespread.

Camacho, like Untalan and other bankers, says debt “when managed responsibly, can have a positive impact on the local economy.”

“It allows individuals and businesses to make important purchases, like homes and cars, sooner than they might otherwise be able to.”

Cruz says using debt to purchase those big-ticket items as well as large household appliances can help “stimulate the local economy.”

“These all contribute to a higher standard of living and a better quality of life. However, if too many people have too much debt, this could become a drag on the economy.

Deliquina warns that too much debt in a community can actually cause an “increase in business operational cost, increase in cost-of-living, and even underemployment.”

Flores says, “Responsible spending and borrowing play a crucial role in supporting the local economy and maintaining financial stability.”

“When individuals borrow within their means and use the funds to invest in the community, it can have positive ripple effects,” he says. “However, overextending oneself can lead to financial strain and potentially destabilize one's financial situation, which can have negative consequences for both the individual and the wider community. It's essential for individuals to assess their financial capacity and make informed decisions to avoid such scenarios.”

So then what happens when debt becomes too much to handle?

“For anyone facing financial challenges, a good first step is to go to your trusted financial institution and speak to your loan officer,” Camacho says.

“They will provide you with sound advice on loan management and restructuring. Most financial institutions provide a variety of online budgeting tools, some even offer the ability to monitor your credit score and offer tips for improving it. For ongoing education, consumers can explore many podcasts, books, and articles on personal finance.”

Flores says BankPacific has an SOS program.

“The last thing we want to do is bring a person to court, or take a car, we want to work the person. We saw a lot of that after Typhoon Mawar. We saw a lot of that during COVID, where people with good credit suddenly were headed towards bad credit,” Flores says. “So, you work with the customers to get them out of that. You want to do everything you can to help customers with financial difficulties.”

Deliquina says there are various programs including those that teach financial literacy that could help keep consumers from defaulting on loan payments. He also lists various government subsidies and assistant programs that can help consumers pay for everything from food to rent to childcare and utilities. Financial counseling is also good before an individual falls behind on payments But there also are debt consolidation programs, and financial counseling.

Cruz adds that anyone who needs help getting back on track can also talk to their primary resource; that is, “the financial institution that owns the debt.”

“Most financial institutions want to assist and will work to find ways to make a loan work,” Cruz says. “The best advice we can give is to be upfront and honest with the lender. They are motivated by your success as it relates to your loans.”

Just as loans are a tool that can help the average consumer afford a home for their family or purchase an automobile that in Guam is a necessity, entrepreneurs and owners or managers of large businesses can use loans as a tool to start or grow their business.

“Debt plays a pivotal and important role for businesses,” Camacho says. “While improper debt structure can strain cash flow and increase risk, when structured properly, debt can also fuel growth and expansion. Debt allows businesses to leverage future expected cash flows now to take advantage of many types of business opportunities like filling a customer’s purchase order or purchasing equipment for improving efficiencies.”

Camacho says the Bank of Guam, as part of its effort to support entrepreneurs, small businesses, and large companies offers a “suite of business products and services.” He says the lack of access to capital is the “primary reason why most small businesses fail.

“The key is working closely with your banker to ensure that debt is properly structured and sized for the requested purpose of the business,” Camacho says. Even down to payments, businesses can choose what options work for them so they “can focus on what they love - growing their business.”

“We understand that flexibility is key, which is why we offer a range of financing options such as lines of credit, term loans, and credit cards for smaller businesses, and specialized services like letters of credit and government-guaranteed loan programs for larger companies,” Camacho says.

Similarly, Flores says BankPacific offers loan options with lines of credit “to help companies when they need working capital, whether it's to buy inventory, whether it's to just to meet payroll this period.

“Or if it’s to get them through the hard times. By understanding the challenges and aspirations of entrepreneurs, we provide tailored financial solutions that support their growth and minimize financial strain,” Flores says.

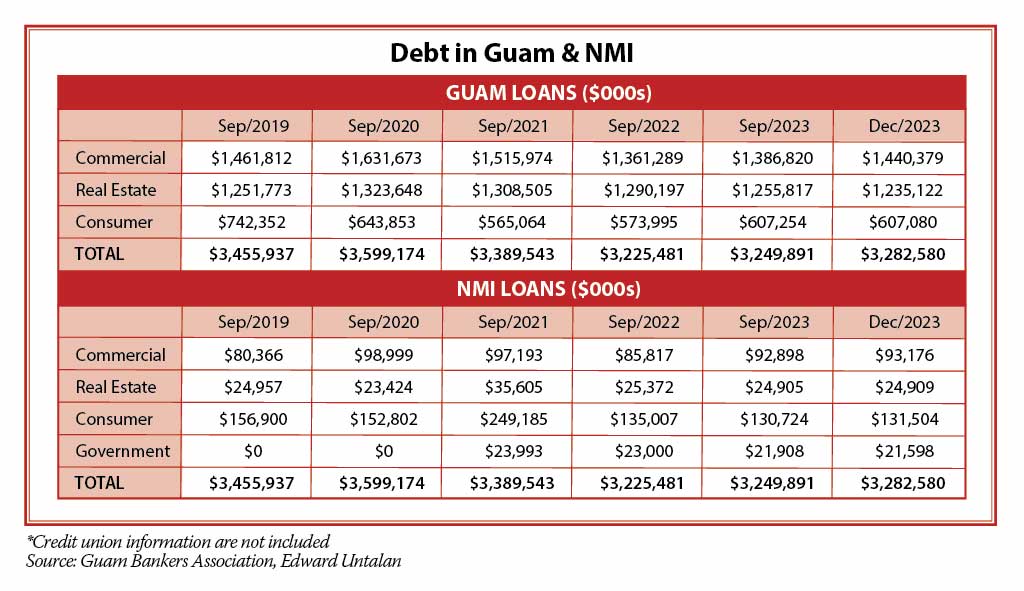

According to the Guam Banker Association Report, there is a total of $1.44 billion in commercial loans, as of the fourth quarter of 2023, Camacho points out.

That’s near the levels seen in 2019, pre-COVID-19, at $1.47 billion. However, a look at the data shows a steady rise in commercial borrowing in 2020 as the pandemic made itself felt, primarily among businesses in the tourism industry. In March 2021, borrowing peaked at $1.66 billion.

Flores says “having access to different levels of financing is essential for businesses at various stages of development.

“For smaller entrepreneurs just starting, a line of credit in the range of $50,000 to $75,000 can provide the necessary capital to launch their ventures,” Flores says. “However, for larger expansions or property acquisitions, significantly higher loan amounts may be required, ranging from millions of dollars.”

Cruz says Community First, like other institutions, also offers a wide range of business deposit and loan products, however, its focus is on industries we understand and businesses we feel we can add value to.

“Consequently, this has meant that our business members are small to medium in size, usually locally formed, and in the housing, small to medium construction and development, small retail, service or medical field,” he says. “The commercial business market is not homogeneous, like the consumer market. Proper debt levels are relative to the industry, the individual business and the position that business plays in the space they compete in. In addition, the use of funds will determine the type of loan a business may need. Levels will range from $50,000 to a few million.”

Camacho and other industry leaders say the most common sources of business debt for local businesses are loans, credit cards, vendor financing, government loans and commercial mortgages from commercial banks, credit unions and finance companies. The debt is used to expand the business or purchase inventory, equipment, land, or buildings.

And while entrepreneurs and large businesses alike borrow from various banks and credit unions, there are a few “large players that have the ability and capacity to go directly to the capital markets for funding,” Cruz says.

“I suspect this may become more common as private asset managers and institutional investors become more comfortable with private debt as an investment option and interest rates become more attractive to borrowers by removing the intermediary,” Cruz says.

Deliquina says there’s been much activity locally that has spurred borrowing, and has in turn contributed to Guam’s economic growth. He lists military buildup construction results in “construction companies needing additional working capital.” He also says Coast360 is seeing more start-up businesses taking advantage of new opportunities and property development companies borrowing to fund projects as the economy recovers. The real estate industry also is a big part of that growth as housing demands are increasing.

Challenges in Guam include the higher cost of doing business and higher interest rates, Untalan says.

Similarly, Deliquina says the high interest rate, disruption of supply chain that impacts the importation of goods and raw materials from the mainland U.S., shortage of skilled workers, high operating costs, small and limited market, and unforeseen events like the 2023 Typhoon Mawar that cut down utilities on island, all impact businesses and the bottom line.

Deliquina says because Guam’s economy continues to rely heavily on tourism and construction industries there’s a natural limitation that comes with that.

However, just as businesses can use debt to start or expand their businesses, they can also use it to bridge gaps. “Debt used as an investment vehicle or a means to bridge short-term working capital gaps can be an effective way to reach business success. However, business owners need to first chart a business plan and use debt as a means of executing the plan,” Cruz says.

Flores says, just as is the case with individual consumers, banks want to work with customers who have fallen on tough times.

“We never want to repossess vehicles nor are we in the foreclosure business. The last thing we want are cars in our parking lot that we have to get rid of. We’re always willing to work with a borrower as much as we can. However, if the borrower is not, then we’re going to get out as quickly as we can,” Flores says.

“We have the SOS program for all our customers, whether it be for a personal loan or a business loan. If we see that an entrepreneur is working hard to pay off their debt, then we want to be there to support them. I know what it’s like to start a business; it can be very difficult.”

Flores reiterates the need to foster a relationship with the chosen banker “from the very start, so that the banker understands what you've been doing, understands your business a bit, and when you need additional funds, the banker will act on it with a lot more knowledge.”

He says it’s OK to deal with more than one bank.

“Diversifying banking relationships and being proactive with borrowed funds wisely are sound strategies for managing debt effectively,” Flores says. He also imparts a bit of advice, saying business owners should “build a nest egg.”

“This way when you look for more line of credit, the bank has you on record showing that you’re devoted and committed to your business,” Flores says.

Cruz says bankers don’t manage business debt for a business or the region.

“We see ourselves as a facilitator and work with the business owner to provide the necessary capital for them to carry out their business plan,” Cruz says. “In doing so, we look at the feasibility of the business plan as well as an array of items in the business, its industry and the island. This analysis provides the comfort level we need to make an investment in the business.”