Adapting to trends in banking and finance

By Joy White

Guam and Saipan banks are keeping up with trends in technology, regulations and customer needs to grow with the community.

BankPacific is hoping to roll out two new products by the end of the year, Bank of Hawaii recently introduced Cardless Cash, which allows customers to use their mobile device to withdraw from their checking account linked to a debit card or bankcard at select Bank of Hawaii ATMs and the Bank of Saipan is upgrading its systems.

“We recently completed a core system conversion, which will provide the platform needed to expand our product and service offering, and increase customer convenience,” says John Z. Arroyo, president and CEO of Bank of Saipan.

John Wade

First Hawaiian Bank launched its initial public offering on Aug. 4, 2016 on the NASDAQ Stock Exchange (NASDAQ: FHB) and with the market cap valuation of $3.2 billion, it became the largest publicly traded company based in Hawaii.

On the economy, the banks note that labor continues to be an issue.

“We are seeing project delays in industries where the type of labor is not available or is undesirable. As on Guam, the probable consequence is higher labor costs, as these workers are sourced through nontraditional channels,” Arroyo says.

Lourdes Leon Guerrero

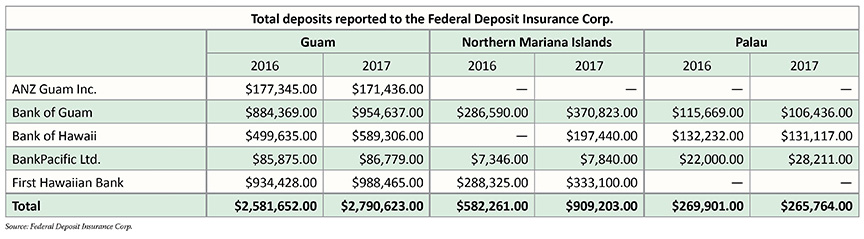

Bank of Guam’s data shows a 5.4% unemployment rate in Guam, with a shortage of construction that is inhibiting the island’s development, says Lourdes A. Leon Guerrero, president, CEO and chairwoman of the Bank of Guam. But the bank is seeing positive change in the NMI. “The CNMI, though, has recovered nicely from their most recent recession,” she says.

Also in the NMI, banks report a growth in loans and increased savings demand, as well as more real estate activity as part of the trickledown effect from the gaming facility built by Imperial Pacific (CNMI) Inc.

Banking institutions, along with other industries, await improvements in telecommunications in Palau, which will improve the ease of doing business, as well as provide more access to online Services.

Guam Business reached out to major players in the banking and finance arena to update movement in the economy and industry.

GBM: Branches in Guam still seem to have considerable lines of people who prefer to be served in person. Is this a true reflection of consumer preference?

John W. Wade, CEO, American territories, ANZ Guam Inc.: I think it’s [about] people who adapt to technology. Technology has been adapting as people adapt. I think you’ll see less and less people in branches. I think the younger generation are more adaptable in relation to technology and using their phones as a tool.

Leon Guerrero: This is a fairly accurate representation of consumer preference, and Bank of Guam views those preferences as a very strong competitive advantage for the organization. In Guam, we have the most number of branches and ATMs, and our online banking and telephone banking services are convenient and competitive. This provides the type of banking channel each customer needs for their particular financing requirements when wanted.

Our island and region have progressed significantly as all payment systems have grown. Automated payments, checks, card payments, online banking payments and more all continue to grow. As with the availability of different channels to serve our customers, we also are very up to date with the different channels that our customers choose to use to make payments.

[…] Our Palau branch is doing well, and we have invested in the community through a physical expansion of the branch, which has just been completed. The branch has more than double in size, and we upgraded our ATM.

John Z. Arroyo

Arroyo: Over the years, much has been said and written about the significance of brick and mortar branches in light of new technology designed to improve the delivery of banking services. While customers can accomplish many of their banking needs without having to step into a branch, branch banking has not diminished or disappeared as some had predicted. The reason, I think, has a lot to do with customer access to, and confidence in, electronic banking, the security one gets when dealing directly with a human being and the social aspects of branch banking. In general, I believe most customers prefer to conduct banking business in person. I expect this will shift somewhat as more tech savvy millennials and gen Ys become bank customers, but I don’t expect branch banking to go away. It will evolve to fit the norms and standards of consumers that have grown up digital.

Flores

Philip J. Flores, president and CEO, BankPacific Ltd.: We probably have three or four times more customers than we did 15 years ago, but our lobby is only a third as busy as it was back then, because you go to the bank [on your phone] and you go to the bank on your computer. So, we see a lot more people using their mobile devices to do business with us.

Palau, as far as our offices, is by far the busiest. That’s because connectivity in Palau — it’s not even 20th century — it’s 19th century because they’re on satellite. But they’re hoping to be connected to a cable system by the end of the year. We expect that connectivity will be much better in the next six to eight months, and at that point people will start to use their computers more and start using their smart phones more, and I expect that we’ll see a lot of our customers using devices instead.

Alegre Erlinda

But there are still people that just want to come and do the eyeball to eyeball, because money is your most emotional possession, and some people just want that emotional attachment to a person. That’s on the deposit side or the operational side.

On the lending side, it’s much easier for a customer to be able to talk to [a bank representative] as opposed to sending something online. You can send something online to get the ball rolling, but after that you want to have someone that understands you. That really works for us, because we make all our loan decisions here, and for commercial loans, too.

If you’re a company, you want a lender you can phone […] and if you can deal with your same loan officer so that somebody else doesn’t have to come in and understand your business from scratch, it’s much easier for you.

Monica L. Pido, chief operating officer, Coast360 Federal Credit Union: Recent surveys we initiated indicated that in-branch services are the preferred banking channel, followed by ATMs, coming in at a very close second. Online and mobile services are increasing in preference, however, personal interaction with their institution remains the primary choice. While the use of ATMs is the second preferred banking channel of choice, ATMs do not necessarily reduce the number of transactions at the banking centers, as most ATMs throughout the island are primarily cash dispensers, providing quick and convenient access to cash only.

Edward G. Untalan, senior vice president, region manager and Maite banking center manager, First Hawaiian Bank: We still see a lot of customers who choose to come to the branch for their transactions. For some customers, it gives them peace of mind knowing that someone has received their transaction. Other customers come in seeking financial planning advice or want to talk to someone about a loan.

Erlinda D. Alegre, senior vice president, retail banking operations manager in Guam, Saipan and Palau, Bank of Hawaii: We need to meet customers’ expectations on how they wish to conduct their banking, whether it’s visiting a branch or utilizing technology. At no other time in the bank’s history has there been more going on technologically than now. We have definitely seen transactions at our ATMs and mobile banking channels increase year over year. But technology for technology’s sake is not good enough. We have to understand how technology fits into the busy lives of our customers.

GB: Are credit card breaches something that worry customers?

Wade: Customers shouldn’t be worried. If there are fraudulent transactions, the customer is protected.

Leon Guerrero: Data breaches should worry all of us, and cyber security is a top priority for Bank of Guam. EMV is an initiative which provides enhanced security through the reduction of counterfeit cards through an embedded chip on the face of the card. We issued the EMV debit cards in May 2016, and are targeted to issue the EMV credit cards in 2018.

Arroyo: Credit card breaches have significant adverse impact on consumers’ financial health and can take months, sometimes years, to fix. EMV technology works from the standpoint that it protects consumers against counterfeit fraud. The Bank of Saipan is in the process of rolling out these services, and our cards will be embedded with EMV chips.

Flores: Yes. If you are using an EMV card at a point of sale, customer information is not stored on their mainframe. It’s a one-time transaction, but if you’re buying something online, then you’re giving them all your customer information at that point, and if that company doesn’t have a secure firewall, they can be breached.

Tia Borja, marketing manager, Coast360 Federal Credit Union: As technology continues to evolve the way consumers pay, I believe there will always be a general awareness and level of caution among consumers who take these alternative payment options. Perhaps it even causes some consumers to stick to traditional forms of payment. Unfortunately, credit card fraud isn’t the only option of concern when it comes to security breaches. Technology breaches can compromise more than card information. While not 100% fraud proof, EMV chip technology is one of the more recent security enhancements to plastic cards and is currently used in over 80 countries. Unlike the traditional magnetic strip, the chip card is more difficult to counterfeit or copy. Coast360 is proud to offer our members the EMV security chip on all our cards.

Untalan: Credit card breaches are always a risk for customers; however, it is important for customers to be vigilant with frequently monitoring their accounts for any suspicious transactions. Although EMV cards are more secure, it is still very important for customers to take steps to ensure all of their information is safe.

At FHB, we are currently updating our ATM, debit and credit cards with EMV. New EMV-enabled cards are being rolled out in waves and sent out to customers as soon as they are available.

Alegre: Yes. The embedded chip on debit and credit cards provide an additional level of fraud protection for point-of-sale transactions when used at chip-enabled terminals. The embedded chip generates a unique transaction code which prevents stolen data from being fraudulently used. Bank of Hawaii utilizes EMV technology in its debit and credit cards.

GB: How would you describe deposit and loan activity as a reflection of consumer confidence at the moment?

Wade: People are still maintaining and increasing the amounts of deposits they’re holding. We’re seeing positives there. In terms of loan activity, we’re also seeing an increase there. In relation to confidence, housing prices have gone up. There’s certainly a level of confidence, but I’m not sure if they’re more comfortable in buying homes before prices go up or [because the] buildup [is on the horizon.]

Leon Guerrero: I think that deposit activity is influenced by a lot of different factors that go far beyond consumer confidence, so it is quite difficult to segregate the effect of any single factor. However, consumer loan activity is directly related to consumer confidence. When consumers are optimistic about the future, when they think their jobs are secure and their level of income will be consistent in the coming years, they are more willing to borrow money with the self-assurance that they will be able to repay their loans. When consumers are apprehensive, when their outlook is less optimistic, just the reverse is true: they tend to borrow less.

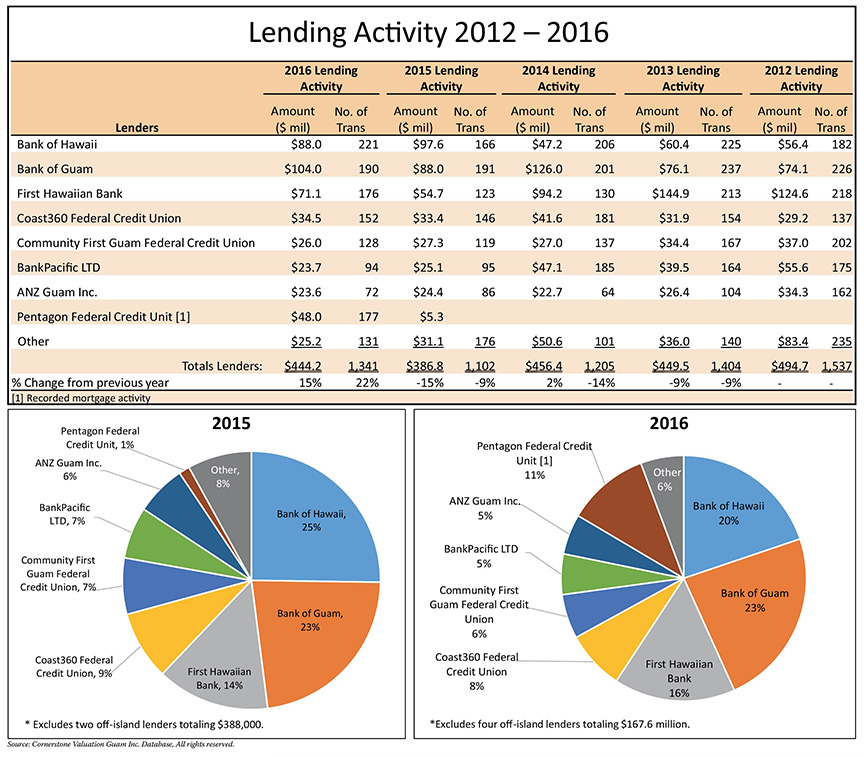

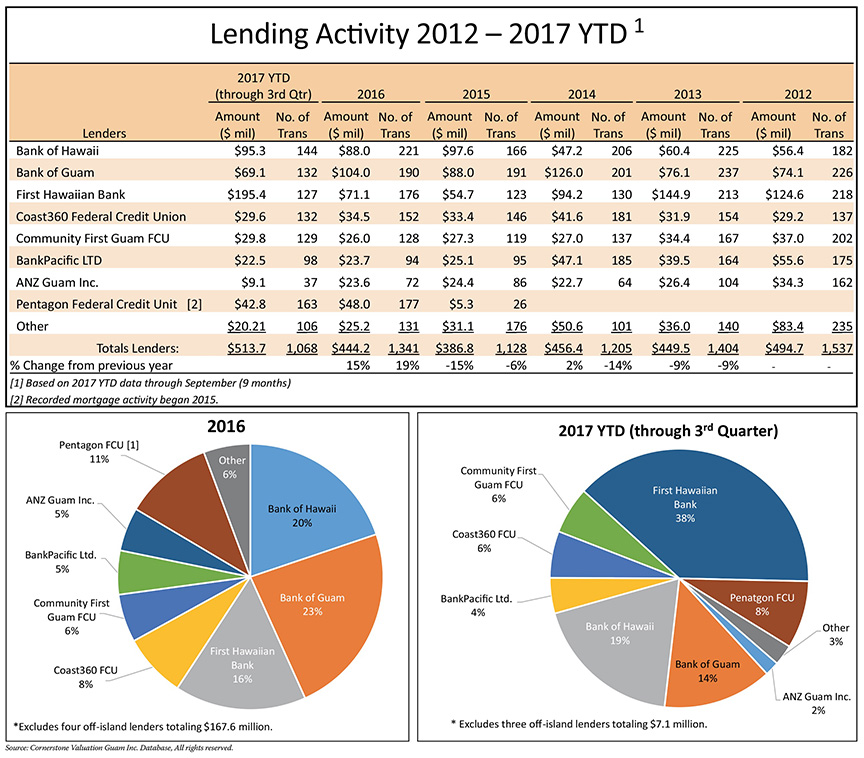

Over the past three years in Guam, consumer loans have risen by $211.8 million, or 35.6%, to $806.6 million, and continue to rise. Similarly, consumer loans in the NMI have risen by $61.8 million, or a remarkable 86.6%, to $133.1 million, and are also still moving forward.

Arroyo: We tend to take on more debt when times are good. Our income is greater and we use extra cash to improve our standard of living. During tough economic times we scale back on spending and, to the extent possible, put away extra cash as a safety net. Today’s consumer confidence in the economy is reflected in greater personal debt. As an example, the loan deposit ratio for NMI banks was 0.3% in June 2012, 0.5% in June 2017. Stated another way, we borrowed $0.03 in 2012 and $0.05 in 2017 for every dollar we held in deposit those years. In actual dollars, the aggregate outstanding loan balance was $67 million and $128 million in June 2012 and June 2017, respectively.

Flores: Consumer confidence was really down in the Obama years because the economy was so bad coming off the collapse of the housing market and with commercial real estate being overbuilt and the number of people out of work for the long term. What we saw then was deposits grow a lot, and that was across the nation — banks being flushed with cash. Part of that is people not having confidence to go and buy stuff — whether it be a car or a house. They would rather accumulate their cash, so our deposits across the nation are really flush. We’re all flushed with money, so it’s a great time to borrow.

Deliquina

Pido: Consumers are placing their funds in short term facilities and core or liquid deposits in anticipation of increasing rates. Deposits are more volatile as consumers chase rates within the market for the best value for their funds.

Gener F. Deliquina, CEO, Coast360 Federal Credit Union: We continue to experience moderate loan growth for consumer spending, an indication of strong confidence in Guam’s economy.

Edward Untalan

Untalan: We still see good deposit and loan activity. Since the bank is backed by Federal Deposit Insurance Corp. protections, customers have confidence when choosing to bank with FHB.

GB: What should the community know about interest rates right now?

Wade: Interest rates are on the way up. They have come up in the past year and a half. The expectation is that over the near to medium future, they’ll probably continue to go up, but not as steeply. But we can certainly expect to keep inflation in check.

Leon Guerrero: I think that the most important thing to know is that interest rates are still near historical lows, so borrowed money is still fairly inexpensive over time. At the same time, low interest rates translate to low yields on deposits and most other financial assets. The good news for savers, and the bad news for borrowers, is that the cycle of monetary policy has started reversing course. The national unemployment rate is near the lowest it has been in nearly a decade, and although the rate of inflation is still subdued, it is just a matter of time before shortages of labor and other resources begin driving prices upward.

The Federal Reserve’s Open Market Committee has raised its target interest rate twice already this year, and many believe it will raise rates again in December. Although that is not a certainty, the Feds will have to start raising rates sometime soon, and probably at a fairly rapid pace. During the financial crisis, they bought up a lot of financial assets to hold interest rates down, and now they are anxious to reverse course and get those assets off of their balance sheet. That will have the impact of raising market interest rates. In other words, now is a good time to borrow.

Arroyo: Interest rates have increased, although marginally, this year and increases are expected to continue in 2018. Certain loans and investments react differently to rate changes as some respond more rapidly than others. Credit cards, auto loans and adjustable rate home loans and equity lines of credit are examples of loans that react quickly. Anyone considering these types of loans in the near future should act now, or face the possibility of higher rates down the road.

Flores: Interest rates have gone up. The Feds have increased [interested rates] by 100 basis points, or 1%, but that would be reflected in commercial loans or tied up to the prime rate or other loans that are tied to an index that has gone up. If you look at long term money for borrowing, like for a home, they have gone up very little, if at all and rates are still, overall, extremely low. So, if someone was going to go out and make an investment, whether it be a car or a house or a business, it’s a great time to borrow.

Deliquina: Interest rates have reached its bottom line. We have seen the last two rate increase by the Federal Open Market Committee and expect more to come gradually. Today is still a good time to buy a house, refinance a mortgage or buy a car.