Nino Eduard G. Aquino

Partner

Ernst & Young LLP

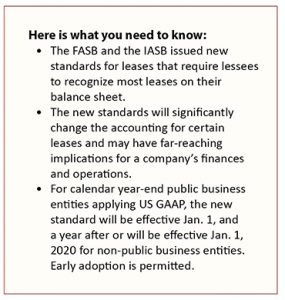

The Financial Accounting Standards Board and the International Accounting Standards Board, the accounting standards setting bodies of U.S. Generally Accepted Accounting Principles and International Financial Reporting Standards, respectively, each issued a new lease accounting standard. Both the FASB’s and the IASB’s new standards will require lessees to recognize most leases on their balance sheets as lease liabilities with corresponding right-of-use assets. However, the standards are not fully converged due to different decisions reached with respect to lease classification and the recognition, measurement and presentation of leases for lessees and lessors. These differences could result in similar transactions being accounted for differently under GAAP and IFRS. For example, the expense pattern for most of today’s operating leases would be different. This article focuses on the FASB’s new leases standard (the new standard).

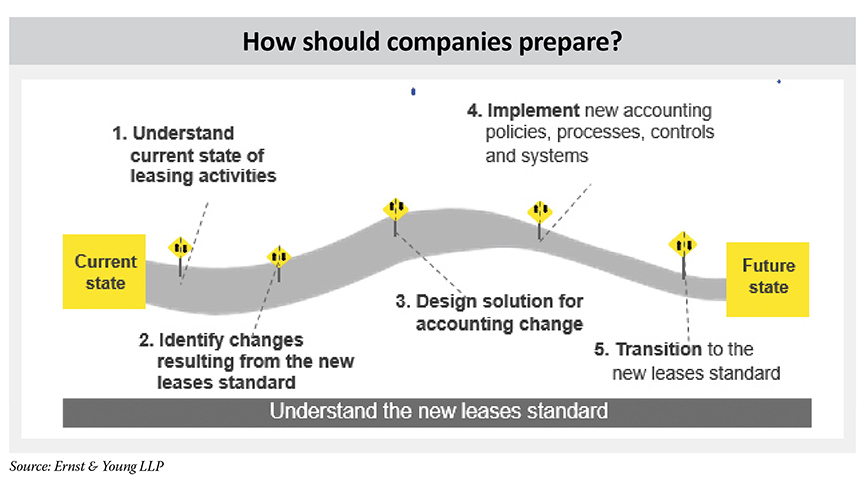

So, what does this mean for your company? The new standard brings a wide range of implications across the organization. It is imperative to understand the full impact in order to avoid challenges down the road.

What is the impact for lessees?

Leases play a critical role in the business operations of many companies. However, because most lease transactions (i.e., operating leases) are off-balance sheet today, accounting for leases under the current leases standard often does not require a significant effort. The new standard will require a company to do more than simply convert its existing operating lease commitments footnote disclosure to reflect lease assets and liabilities. In many cases, it would result in changes to the policies, processes, controls and IT systems that support lease accounting and possibly lease procurement, lease administration and tax. Companies may also want to consider the implications to financial statements and metrics as they negotiate contracts that are, or may contain, leases.

Accounting policies and procedures

Accounting policies and procedures

The new standard requires the application of judgment and estimates. For example, for certain arrangements such as contracts that include significant services, evaluating whether the arrangement meets the definition of a lease could require significant judgment. The revised definition of a lease could result in some arrangements receiving different accounting treatment compared to current guidance. The elimination of the “bright-line” tests associated with lease classification could also result in the need to apply judgment. Other key decisions requiring judgment include lease term and lease payments, including reassessment of lease term and the accounting for lease modifications. While the FASB expects many of the conclusions to be the same under the new standard, many of the judgments and estimates may receive increased scrutiny because lease assets and liabilities will be reported on the balance sheet for most leases.

Also, there are a number of accounting policy elections that may be taken both at transition and for the accounting post-transition, including whether to adopt a short-term lease recognition exemption. In addition, the new standard allows for certain transition reliefs that, if elected, can help minimize the implementation burden. Companies will need to understand the impact of these options to help in making informed choices as to which election to make.

Companies will also need to update their policies, procedures and internal controls, as well as provide education and guidance across the organization in order to ensure accurate and consistent policies and processes around areas of judgment and estimates.

Financial statements and metrics

For most lessees, the new standard will result in a gross-up of the balance sheet. This could cause a deterioration of debt ratios and return on assets as compared to current lease accounting. For example, regulatory capital of lessees that are financial institutions also may be impacted. This will likely depend on how regulators react to the new standard.

A company should assess the potential impact on its financial statements and metrics and evaluate how this may affect the way stakeholders view the company’s financial performance. Companies will likely need to educate internal and external stakeholders on the implications of the new standard to the company’s financial statements and key performance indicators.

Tax considerations

Adoption of the new standard will result in additional tax-related considerations. These include understanding initial adjustments to deferred taxes and tracking book/tax differences. Companies will need to determine necessary changes to tax-related processes and controls required to identify and track tax adjustments.

Are there changes for lessors?

While many aspects of lessor accounting under the new standard are expected to remain the same, some lessors may still experience changes. The elimination of today’s real estate-specific guidance (e.g., the requirement for transfer of title for a sales-type leases involving land) and changes to certain lessor classification criteria will result in more leases qualifying as sales-type leases and direct financing leases.

However, profit recognition for certain direct financing leases (typically equipment leases in which third-party residual value insurance is used to meet the 90% present value threshold) will now be deferred to align with the criteria for a sale in the new revenue recognition standard whereas losses will be recognized.

Changes to the definition of initial direct costs will also impact the calculation of a lessor’s implicit rate and result in more costs associated with entering into a lease being expensed up front. Similar to lessees, lessors will also have new disclosure requirements.