Business loans and investing heat up following the release of federal military buildup funds, though some banking industry icebergs must still be circumvented.

By Bryce Guerrero

The U.S. financial crisis of 2007 is looking to be the darkness before the dawn of Guam’s economic growth — at least that’s what Guam’s banking executives anticipate and what everyone hopes. As federal funds for the military buildup are unfrozen and the money gets flowing, Guam’s economy shows signs of progress that these bankers believe will only grow in the coming years.

With economic stimuli including portions of tax returns being paid to residents sooner, many of Guam’s banks are seeing significant growth in deposits. Bank of Guam president and CEO Lourdes A. Leon Guerrero says, “We definitely saw in our bank a major increase of our deposits. […] From December 2012 to December 2014, our total deposit base grew by over $150 million.” She estimates that from December 2012 to now, Bank of Guam’s deposit base has grown to more than $250 million. Similar trends are noticed throughout Guam’s banking industry.

“With the government’s commitment to dispersing tax refunds timely [and] also the [Cost-of-Living Allowance] — that’s generating a lot of savers — [people are] depositing. If they’re not saving the money or depositing it into savings accounts, they [are paying] off their loans,” says Gener F. Deliquina, Coast 360 Federal Credit Union’s chief executive officer, who has observed that the credit union’s members are paying off their loans earlier using their tax refunds.

Gerard A. Cruz, president and CEO of Community First Guam Federal Credit Union, agrees that tax refunds, as well as government pay increments, are contributing to an upward trend in deposits. “These circumstances have had a great effect in growing deposits,” he says. The trend was also aided, he says, by the exit of Citibank, a major player in the local financial institution market, in 2014.

When excitement over the initial announcement of the military buildup began, many banks on Guam saw substantial loan increases from businesses that were prepping for unprecedented growth. But when the buildup was prolonged, many projects were abandoned, ghosts of which can be seen intruding on Guam’s skyline.

“I think everyone here was banking on the fruition of the military buildup. […] I think it’s picking up steam again. It’s more realistic now with that recent release of the funding,” Deliquina says, noting Congress’ lift a nearly four-year freeze set on funding for the buildup.

Though the buildup proved to be a letdown after its initial announcement, Ronald E. Cannoles, executive vice president and Pacific islands division manager for Bank of Hawaii, says he sees some blessings in disguise from the delay.

“In a positive way, [the delay] gave the Department of Defense, [Naval Facilities Engineering Command and] all the parties that are involved more opportunity then to go and address the community’s concerns,” he says.

Since the economy has stabilized and government plans have become more concrete, loan trends tell of a resurgence of businesses that are again looking to accommodate the expanding market.

“When they first announced the military buildup, there was a huge amount of business loans, investors coming in trying to look at setting up shop, but because it’s been prolonged, it’s kind of trickled out. Now we’re starting to see some more activity coming about,” says Laura-Lynn V. Dacanay, senior vice president and Guam and the Northern Mariana Islands region manager for First Hawaiian Bank.

The numbers at Community First Federal Credit Union support this observation as well.

“In 2013 we closed the year around our typical average; however, in 2014 we ended the year with a 29% increase in business loans funded,” Cruz says.

Guam’s banking executives have noted trending increases in subcontractors looking to increase their working capital lines, office space and housing.

John W. Wade, CEO of American territories for ANZ Guam, says he has noticed an influx of activity over the past five months. “Some of it is anticipation of the buildup. It seems like there’s an increase in housing with the intention to rent to military,” Wade says. At the first notice of the buildup, there was a “euphoria” that prompted people to build, but they were let down when the military decided to restrict their personnel to on-base housing.

“But it seems now the base housing is full and people are now going back outside the base. […] That bodes well for the economy, the military and the non-military, and it bodes well for jobs.”

With Guam’s economy pressing forward, now seems like primetime for businesses to invest in developments and renovations. Cannoles says individual businesses need to determine if investing in developments and renovations would be profitable on a case-by-case basis.

“What I would say is that it’s a very favorable time to take on debt. We’re at historically low interest rates for borrowing. So that’s helping both our commercial customers as well as our consumers, particularly in the residential mortgage space, where homes are more affordable because the interest rate is less expensive.”

Philip J. Flores, president and CEO of BankPacific, says, “If you ask me, ‘Is it a good time to invest in Guam?’ I’d say, ‘Absolutely, yes.’”

Leon Guerrero says that Guam’s economic state is a good platform for innovation and the introduction of products and services.

“As your economy gets better, this is a good time for people to look at expanding their services or even bringing in new services that maybe we don’t have here, being much more creative in the types of delivery of services that they may feel is not being delivered,” she says. “I think it’s an opportunity for people to be looking much more at the community and saying, ‘What is the community wanting?’”

In real estate lending and developments, specialists foresee continued growth as well.

“The military buildup represents a good opportunity for people to invest in the rental real estate market, which remained strong through 2014 and which offers good potential for 2015 and beyond,” says Eric Hodnefield, senior vice president and residential sales manager for Finance Factors. “We anticipate growth in this area, especially for entrepreneurial-minded investors who are willing to build and rent.”

However, federal regulations imposed on real estate lending have made the process burdensome.

“What we all feared [would] happen has happened. The Dodd-Frank banking format — it’s a nightmare,” Flores says. “One of the things it’s done is made it harder for individuals to qualify for a home loan.”

President Barack Obama signed the Dodd-Frank Wall Street Reform and Consumer Protection Act in July 2010. The regulations included were intended to protect homeowners from loan programs they were not qualified for, but the regulations have had

negative side effects.

“The unintended impact of the new rules was a dramatic increase in paperwork and documentation required from borrowers, which added time and complexity for even well-qualified customers,” Hodnefield says.

Dacanay says many banking institutions are struggling on the residential lending side because of the regulations and that reporting compliance to the various federal agencies requires more personnel as the regulations become more complicated. She says First Hawaiian’s compliance division went from being staffed by about three people to more than 20 people because of the strict protocols.

Nevertheless, many of Guam’s banks are reporting stable, if not prospering, real estate activity. This is thanks to interest rates being at a historical low. Refinancing is prevalent, and demand for new homes continues to grow due to the low rates.

“Certainly on our residential consumer mortgage business, it was quite a busy year for us,” Cannoles says. “We did upwards of $27 million just purely in residential loans. That was a combination of people refinancing their existing loans […] and then new entrance into the market — people buying homes for the first time. Because of the low interest rates, the homes have become more affordable for a larger section of our population. And then investors have been fairly active in the real market as well, so I think the real estate industry as a whole did fairly well in 2014, and I only think that’s going to get better as we move forward, particularly if we get the record of decision.”

Because of the low rates, consumers have a lot of incentive to borrow, whether for personal loans, to consolidate debts, to pay off credit cards or to finance vehicles. But according to Dacanay, there are not many incentives for consumers to save.

“Because the borrowing rates are low, the savings rates are even lower,” Dacanay says. “[…] The rates are more attractive on a long-term basis versus putting it in a savings account. […] You can get a better rate on a timed deposit, but some people prefer to keep it in a savings account or short-term timed deposits because then the money is more accessible to them.”

And because the rates are at a historical low, the only way for them to go is back up.

“Everybody anticipates rates to go up. It’s really just when will the feds pull the trigger,” Wade says. “In terms of savings, I think people are still cashed up, but I’m not seeing a lot of people putting out any longer dated CDs — or certificates of deposit. They’re pretty much keeping it short, presumably in anticipation of rising interest rates,” he adds, echoing Dacanay’s observation of savings.

A new regulation on the federal level that may have an impact on lending in Guam is a consolidated Good Faith Estimate and Truth in Lending form, which Hodnefield says goes into effect Aug. 1.

“Lenders and escrow companies are currently working very hard to understand the rules that go with the new forms and to integrate the new forms and rules into their lending and escrow software systems,” Hodnefield says. “The good news for the borrower is that understanding the terms, costs and conditions of their loan should be clearer than ever. The potential downside of the new form is likely longer closing times for loans, as one of the rules requires that the borrower be given the new disclosure three business days prior to closing their loan.”

The additional days are so the borrower has ample time to review all of the transaction information and costs, he says, “but it will extend closing dates, as the current rule requires a one-day review, which can be waived by the borrower.”

Saipan is expected to mirror Guam’s growth in development, albeit in a smaller fashion.

“Business loans in Saipan are fewer. Their economy is still struggling, but there’s been a lot of positive signs in Saipan,” says Dacanay, who also highlighted the projected casino investment that will be pumping millions into Saipan’s economy.

Real estate transferal is a challenge on Saipan. Article XII of the NMI Constitution requires landowners to possess at least a fraction of Northern Marianas descent in their heritage, so the bankers have not seen very significant increases in Saipan’s real estate market.

But Flores says he sees Saipan’s economy as a very impressionable one, easy to impact.

“You do see now an investment in Saipan. Their tourism has grown the last couple of years […]. Saipan is just this little demitasse — this little cup — and [if you] spill it, [it] leaves it empty because it’s so small, but on the other hand, it doesn’t take very much to fill it back up,” he says.

Consumers are able to view account information and make purchases, put down deposits and withdraw hard cash all at the stroke of a key or a swipe of a finger — from virtually anywhere in the world. But along with electronic banking’s obvious enablement comes the growing risk of cyber security.

“With the numerous fraud alerts and security breaches going on nowadays, financial institutions are expected to develop and implement programs that protect their customers’ sensitive information. We can expect major changes to the regulatory landscape because of this,” Deliquina says.

Identity theft scams are growing to be more and more complex and well-disguised, while consumers’ ignorance or naivety further opens the doors for cyber attacks.

“I think the challenge that we find as an industry is that these hackers are very sophisticated, very smart, and it’s challenging to stay ahead of them,” Cannoles says. “I think U.S. banks in general have built sufficient and very robust security systems around their networks to secure our data. […] I don’t think the community needs to worry about cyber hacking into the banking system. I think where they really need to keep their guard up is with these advance fee fraud schemes and different types of frauds that are perpetrated over the Internet. […] If I was to say anything, I would caution the community about responding or clicking on any links.”

Leon Guerrero says technology and the media through technology are here to stay. “And it’s only going to expand more because people want quicker convenience — information at their fingertips. But there’s a price to pay, too, and that is your security. People need to make sure their laptops are secure […]. They need to be educated.”

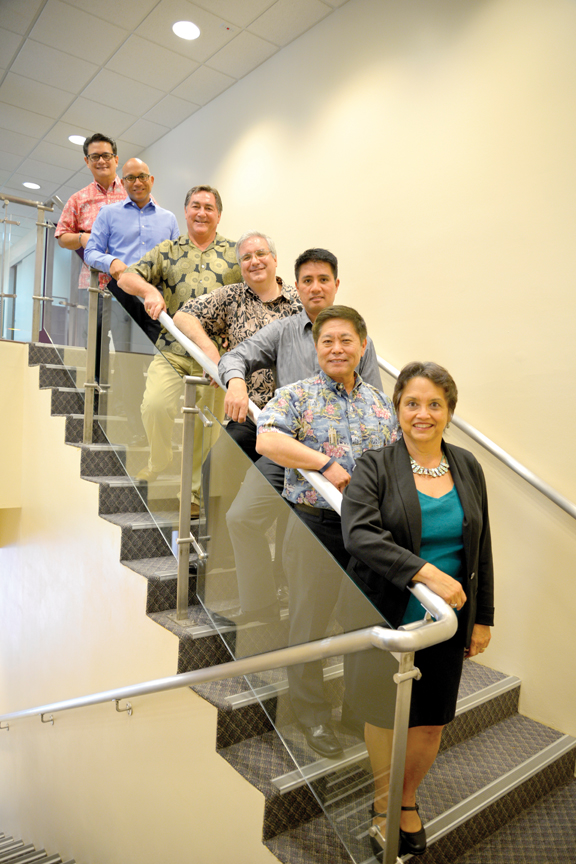

(From left) Edward G. Untalan, senior vice president and Maite banking center manager, First Hawaiian Bank; Gerard A. Cruz, president and CEO, Community First Federal Credit Union; Philip J. Flores, president and CEO, BankPacific; John W. Wade, CEO of American territories, ANZ Guam Inc.; Gener F. Deliquina, chief executive officer, Coast360 Federal Credit Union; Ronald E. Cannoles, executive vice president and Pacific islands division manager, Bank of Hawaii; and Lourdes A. Leon Guerrero, president, Bank of Guam.